You can also view both the slides and the video on the district website.

(for these notes, you’ll need to look at the slides along with the notes)

Call To Order: All Board members present

Pledge of Allegiance

Budget Presentation

Budget Process Overview

Board approves at the expenditure function (legal level)

If actual expenditures exceed budgeted, then it goes to the board for approval

Each project’s budget managed by the district within the board approved function level

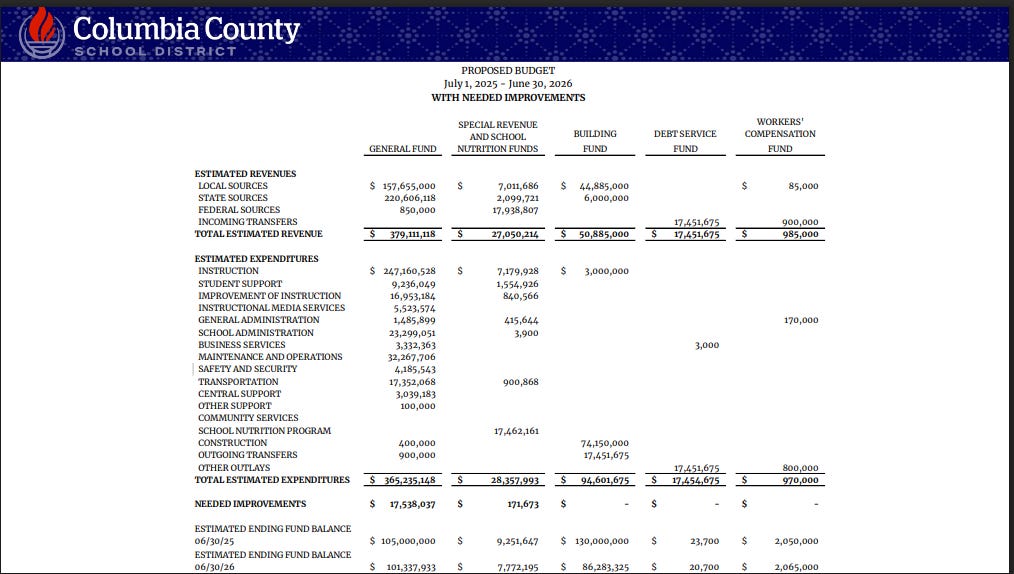

Proposed Budget

When there is a change in expenditures above revenues, it builds reserves.

Will reduce reserves a bit for improvements this year

Some are ongoing expenses into the future(such as salaries) and some are 1 time

Additional laws, such as the new safety bill, are unfunded mandates - still assessing.

General Fund

Shows the success story of having a high performing district with a fiscal conservative board.

Majority of expenditures are spent on instruction.

Salaries/benefits are above market making district competitive

Employee numbers are re-totaled with improvements

Major Increases

Step Increase - $3.3 million

State Health Insurance

Non-certified personnel insurance is not supplemented by the State

Teacher’s Retirement System - $2.1 million

25% increase in insurance, mostly property insurance.

General Fund Improvements

Recommendations

5% cost of living increase in salaries (in addition to step-increases if not maxed out on step-increases)

Total Inflation since 2020: 24%

COLA since 2020: 12.9%

Total: $12,234,784

#2-17 on requested needs list

Fund some expenditures by spending down general fund balance

#2 on the list technology - $3 million

$1 million computers

$2 million tech - physical security

2 student advocacy specialists (part of school safety bill) - may be partially reimbursed by the State

School Nutrition

Meant to be self-sustaining

Covid Supplement

Had to spend the fund balance down - replacing aging equipment.

Didn’t lower the fund balance enough

-$1,321,322

School Nutrition Improvements

Last increased price in 2023

Will need to phase-in price increases over the next 2-3 years.

$3.10 to $3.50 lunch; $1.50 to $1.75 breakfast

$4.25 is suggested price and will need to move towards that

40% of students in district are eligible for free or reduced meals.

Improvements

Increase SNP Assistant Pay to Market

Add 5 floating reserve positions

Assistant Managers (17)

SNP Procurement

School Nutrition Training Specialist

Manager Tier System

Kent: What is the optimal fund balance?

Casado: 3 months of operation expenditures - $4.5-5 million

Baker: How many free/reduced vs. paid? Would that offset.

Casado: 40% of the student body is eligible for free or reduced lunch. If the federal government increases their reimbursable rates then that could help.

Special Revenue Funds

Flynt: These are Grant amounts but not total expenditures.

Casado: Special education - $4.9 million shown is just federal $$. State & Local also funds SPED.

5/6/2025 - 2nd Meeting for public input

(It was difficult to follow this discussion because not everything referenced was shown to the public. I will update the notes with Ms. Allen’s document tomorrow when I receive it. I had a conversation with Mr. Casado and clarified some of the content.)

Allen:

Numbers are different from what she saw the night before.

The budget influences the tax-rate for the next year.

She looked at the numbers from the Financial statements the past 4-5 years.

Original Budget revenue vs. actual revenue differences

Actual Revenue 11% above expenditures. Where is that shown on the budget?

Casado: Fund balance at the end is the beginning balance for the next year.

Allen: 2023-2024 Categories

Casado: Schedule 1 in financial statements is different than General Fund briefed at the meetings. Schedule 1 on the statements includes special revenue and school activity accounts. School activity accounts (sports, PTA, individual school money, etc) are impossible to plan for or budget for. The audited statements are different than the budget so it’s not an apples-apples comparison.

Allen: There is $12 million in excess each year. 11% higher revenue. In the past, $12 million was moved to the capital fund. The taxes increased over the past years. So, the patterns of taxes going up and general fund increasing, in excess of revenue. If we have the mindset to set revenue at 3% then side by side comparison.

Flynt: During COVID, there were more federal funds. There were many discussion about how to spend the increase in revenue. There was an increase in State revenue too. At the same time, there was dramatic inflation (40%) in the building program. Within 2 years, we redid the 10-year plan to make adjustments to the building plan.

Allen: The board at that time had discussions and made decisions. What can we do to fund operations, while sticking to the inflation rate for tax increases?

Dekle: Employee salaries are lagging inflation though, right?

Allen: Salaries were raised above inflation in 2023 and 2024.

Dekle: Inflation was higher in other years though according to the chart. (Overall employee salaries did not keep up with inflation.)

Teasley: Inflation was not 3% for the building program and….

Allen: I think it is a false dichotomy. We approve the budget at a large level. There is already extra built into the budget. We can still have excess if we kept the rate at 3%… budgeted revenue only by 3% increase.

Flynt: We builder this budget on a 3% increase and 2% growth.

Allen: 2024-2025 budget…. so many numbers. Budget reflecting 1.3% Why did the fund balance grow at a high rate? Concerned that building the fund balance and shouldn’t be treated like a slush fund.

Teasley: Not taxing at a higher rate. We lowered the millage rate.

Allen: Millage rate was lower but the taxation rate increased.

Teasley: We control the millage, not valuation. There are 3 entities. Our role is the millage rate and we keep our portion as low as possible. It would be better if we saw these numbers ahead of the meeting instead of new numbers at the meeting.

Allen: Annual *didn’t catch*

Teasley: Tentative is not final.

Flynt: We’ll update the website with the latest numbers after the meeting.

Dekle: 3% inflation, 2% growth

Casado: We also had an increase in exemptions last year which more than offset growth in the county. Not sure about this year.

Dekle: Some numbers we have no control over.

Casado: Different things can change the numbers…. How many employees take/don’t take health insurance. There’s a margin of error due to the size of the budget. We assume certain conditions but we don’t have a crystal ball.

Dekle: Include Recommendations

Casado: 3% inflation - property tax, 2% growth. expenditure increase - 5% COLA. Health insurance, TR increased almost double. There are also State mandated costs.

Teasley: Are we required to have an amount of reserve funds by the State?

Casado: Not really anymore, based on policy. Ours is 15%.

Flynt: You as a board have been fiscally conservative compared to other districts. It really is a good news story to have high achievement while being more fiscally conservative.

Allen: HB581 Hearings - It’s always that we have to approve increases or teachers get cut, class sizes increase. The fund balance went up each year. $14 million extra. There’s room to have the best of both worlds. How did reserves keep growing? State revenue increases $220.6 million. I’m not seeing an either/or situation. We keep running at a surplus and we shouldn’t continue to run at a surplus.

Dekle: For the millage rate - we’re discussing the budget right now, not the millage rate.

Allen: The budget is the predecessor though. $14 million surplus comes from the operating budget.

Teasley: HB268 is full of unfunded mandates. We don’t even know what the State will fund and what they won’t.

Flynt: State revenue fluctuates. State revenue rises because of lower class sizes. We give schools what they earned. State revenue increases, scheduling gain funded.

Allen: State or local all goes to the same general fund.

Casado: If all federal $$ goes away, school Nutrition fund fails - the general fund bails it out.

Kent: If a surplus exists and their unintended things…. the just have to be explained.

Allen: SPLOST - which major projects is SPLOST covering?

Casado: All active big projects: N Columbia, LSHS, EHS, Harlem…. Always little extra

Teasley: Not just building but there’s always repairs and refurbishing.

Flynt: A lot of work. One project leads to the next project. We should have designs next year.

Allen: 4 major projects this year. Closing out N Columbia ($10-15 million), EHS, LSHS. In 3rd year, SPLOSt outpaced revenue

Casado: The nature of bonds. We take out the bonds, then spend bond proceeds.

Kent: Can we use the SPLOST for tech need #2?

Flynt: It’s budgeted into the future. SPLOST will pay existing projects. Sometimes able to use Splost.

Baker: I like to see many of the priorities I’ve heard from the community on the needs list such as improvements to mental health and safety. Thank you for looking at addressing the needs from the public.

(Karin’s note from discussion with Mr. Casado: The majority of revenue overages are from the State’s budget surplus in year’s past that they decide to send late in the year. There’s no way to plan for that because district doesn’t control it and can’t plan on getting it. Example - During shutdown, they cut the QBE at the beginning of the year but then supplemented later. Also, he always uses a conservative estimate for interest income because he would rather low-ball it than end up not having enough because he misjudged the interest rate. They are planning on spending down the general fund this year but having a cushion can help weather uncertainties throughout the year. It helps the district to be more financially stable if something unforeseeable happens.)

Public Input

Janet Duggan (on the video 1:15:55 - 1:27:13)

This is transcripted.

Good Morning. I’d first like to say that this is a public hearing and I’d like to reiterate what *someone* said at the HP581 public hearings that this is meant for discussion and it’s not a regular meeting where we typically limit 3 minutes.

*Dekle: I’m just asking…

OK. Well, there’s only me and um I had about 3 or 4 comments but I’ve been taking some notes from this discussion and I have some thoughts about that. So, I would like the time to share that and I know you value that because you value making important decisions and you value the public. So, I appreciate that. OK, that said, I have reviewed the audits and I was looking at Exhibit E of the audits and um, in 2020 the ending balance for the general fund was just over $60.2 million. In 2024, it was $121.25 million which is more than double. I have a couple questions about that. In um 2025 there’s not an audit yet but you had a budget that was the final budget and it had a starting or beginning fund balance of $79.25 million. So, uh if you have the answers to these questions um now that’s fine. If not, I’m happy for you to get that information to me prior to the next public hearing. But in 24, the ending balance on the audit from was $121.25 million. And the beginning budget for 2025 was $79.25 million, which is I think roughly about a $50,000 or $50 million difference. And I heard earlier in the meeting today that the ending balance is basically the beginning balance for the next year. So, I’m just curious where that $50 million ended up getting moved or allocated to. *pause* Did you want to address that or do you want to send that information to me?

Flynt: Mr. Chairman, how would you like us to proceed?

Dekle: ummm, if you would just complete your public comments at this time…

OK. All right. And then number…. What is the current expectation for the ending budget for 2025? And the budget has $77.37 million but we’ve noticed a trend where you know the beginning budget has been 50 and 20, 60 at the end $60 million, $62 million, $81 million, from beginning to end. So there’s an increase and a growing trend. Do we expect that to happen this year? *pause*

And you um my other question which you’ve already answered is where is the additional revenue coming from? I appreciate that information during the discussion. S then the other things are that I want to discuss are more about the discussion from today. So there seems to be an extensive discussion about revenue and expenditures and I would happen to agree with Miss Allen that it’s not an either/or and we saw that with HB581 where in that presentation it was like well if we do this, we’re going to cut you know, fire teachers, go on furlough, etc etc and you know I’ve extensively looked at these financials and I don’t think its an either/or and I find that quite honestly in the discussion there seems to be a little bit of a closed mind to even opening up that discussion. Uh there wasn’t a request to vote on it today. It was a request to have a discussion about, an open honest discussion as to whether or noth that would be something that could be done. And I think that’s a fair request. So I look to the school district and I look to the board to to actually have an honest discussion with the numbers to say, can we do that 3% and do that? Now I heard today that it is a 3% plus a 2% growth. So my specific question to Mr. Casado is when you look at 2% growth, can you tell me how that plays it plays into that that rate? Because if there’s a 5% growth or a 1% growth and that that’s a variable that we don’t know, right? We don’t know that until we get that info from the county or the state. So how does that affect this? And is this board willing, if the growth rate is different than what was projected, to decrease the millage rate, to actually equate to 3% plus 2% growth or do we even need to include the 2% growth? So these are questions and I think the numbers need to be presented to this board with those answers to those questions at the next meeting so that can be evaluated honestly. The answer may be no, we can’t do that. But if you don’t actually look at it and uh honor the request of the board members asking that, I find that to be an issue of concern. *pause*

The last thing that I want to comment on is about amending the budget. So, I appreciated at the last meeting that there was the auditor, I’m sorry, I don’t recall his name that did the presentation about the entire audit process and I found that very informative. I thank Dr. Flynt or or Mr. Casado for inviting him in to speak. I think that was helpful. But one of the things that stood out to me and I would like an answer to this as well is that he said that the internal processes um that that are exist the policies for internal controls um you know it helps prevent fraud. It helps prevent all these things. I understand that completely. I think that’s great. It has to you have to have those things. Um so I completely understand that. That all said, he did make a statement that said, you know, if you, and I’m going to use an example, just for 10 numbers, if you have $100 million budget and you know, you’re spending say $120 million or $110 million, 10% 20% over that, that would be a red flag. I understand that. What I don’t understand is if you have a $100 million budget and let’s just say you’re spending $120 million and that’s a red flag. How if you adjust your budget that’s not a red flag. If your original Budget was 100 and you spent 120, why is you still spent 120 from the original Budget? How is that not a concern? So it appears to me that the internal control process that exists actually makes it more difficult to identify variances in the budget that may cause concern.

Now, that may not be the case, but I would like an answer to that as a public taxpayer and citizen of this county as to how that really does accomplish the intent of what an internal control process is for because I don’t see that. I see it actually making easier to have changes in the budget that do not create a concern. And I’m not suggesting that what you’ve done is a concern because I don’t know that. What I’m suggesting is the process for internal controls that you have actually is not helpful in determining that. So it’s very difficult to determine that based on that. Again, this is a discussion that I would like for you to be able to provide me these answers to. And on that note, I’d like to finally say that when you can transfer $24 million out of your general fund to your capital fund and then over the course of 5 years, I think it’s $60 million. And then you have a discussion up here that we might not be able to pay our teachers or we’re going to have to increase class size. um, when you have 11% increase which I learned today which I think I don’t remember the number with a 10 millions of dollars more 12,13, 14 million dollars more on average and that discussion has been asked, can we account for those dollars somehow and keep and not increase our taxes to our community and still meet the needs and there’s push-back on that. That’s a close-minded uh attitude and and that’s not really what the public’s looking for. We’re looking for open discussion for those things to be looked at. The end discuss the end vote may be whatever it may be, but we really need to honor these requests. They are looked at the numbers. I see absolutely no reason why all of the needs that Dr. Flynt has requested for 1-17 cannot be met that they can be met. I see no reason why. I think they should be met. I have no problem with that and I think they can be met ensuring that the tax rate is at the inflation rate of 3%. And on that note, I’d like to comment, Ms. Teasley, that you do have an issue or a misunderstanding, I believe, of the millage rate. And the reason I say that is when we have public hearings for the millage rate, the law states that those hearings are because we are increasing taxes. If you are not going to increase taxes, you don’t have to have a public hearing. And you’ve had a public hearing for the last 4 or 5 years that I’ve been at board meetings, which means, you know, that an intent to increase taxes. And when you vote on the millage rate, the actual number that you vote on for the millage rate is a tax increase. You have not had a full roll back of the millage rate in the last 4-5 years. So to imply that because you have lowered the millage rate, you are lowering taxes or have no control over the property taxes in the assessment. Yes, you don’t have control over the property assessment, but you have control over the actual number that you are voting for the millage rate, which when property taxes go up, the millage rate has to inversely reduce more significantly to not have a tax increase. This is not difficult. The community is not stupid to this. You don’t, we’re not confused. It appears, quite honestly, Ms. Teasley , that you’re confused or trying to be deceptive, and I find that offensive. I’d appreciate you look into that a bit more. Thank you.

Dekle: Ms. Duggan - I would appreciate it if you would not address board members directly like that. I think the public input is for the purpose of addressing the board and I just take offense.

Teasley - It’s not all surprising.

Duggan: Well well, I appreciate your I appreciate your comments and you’re right, Ms. Teasley, it’s not at all surprising either about the comments that you’ve make. Now, I’m I’m sharing that I disagree with her comments and she’s making comments to the public that are inaccurate when it comes to public hearing. So, I think that stands to be corrected. Appreciate your time. Thank you.

Board Comments:

Kent: Appreciates the discussion. He knows that sometimes these discussions can be tense but they’re important to the public so he appreciates it.

Teasley: Conversation is always good.

Allen: Agreed that these are difficult but important discussions.

Meeting adjourned.